Not All Letters Are Created Equal

Not All Letters Are Created Equal

What No One Tells You about Rating Agencies

In order to overcome a question about ratings, you must be able to explain their limitations, then fill the void with more pertinent information that a consumer actually needs.

In my article, "What's Your Number" I ask the reader to think deeply about the statistics, acronyms, professional designations, and other alpha-numeric shortcuts we use in our industry to communicate with our clients credibility, knowledge, and trustworthiness. Such shortcuts must be understood by both parties, even if they don't value them the same: think of the widely-discredited Better Business Bureau ratings which still command inordinate sway with consumers. For an insurance carrier, a 170-page annual report is condensed into a single letter, which becomes the common currency of consumers, agents, and the media. Into this letter grade we pour our trust. Let's examine whether this is wise or practical.

WHAT A RATING MEANS

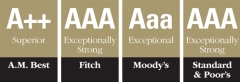

AM Best defines their rating as "an opinion...and not a warranty". Standard & Poor's cautions similarly theirs is "an opinion...not a guaranty...and not a recommendation to purchase." Moody's likewise warns that their ratings constitute but "an opinion".

Then there’s infamous Weiss: “Other rating agencies give top ratings more generously so that most companies receive excellent ratings. While this approach provides great marketing material for insurance companies and helps agents and brokers sell more insurance, it doesn’t help the user....” In spite of its self-appointed role as contrarian and consumer-watchdog, independent analysis confirms Weiss is not a tougher grader. Worse, Weiss is literally immaterial (deemed irrelevant to investors), a fact which renders the popular Comdex Score un-usable for unwisely including it.

For the majority of producers, decades of our careers will be spent representing a bandwith of carriers from within the "SECURE" categories. Still, as many as 77% of companies may fall into this band, a veritable “Circus of Heaven”. Meanwhile, the rating agencies are in the peculiar position of having been ceded extraordinary power with little risk. To wit: according to a 2012 report, the number of Life & Health impairments has reached a 50-year low. In general terms, this means identifying a high-quality Life & Health insurer is no more difficult than hitting the broad side of a barn.

Several years ago, AM Best Life & Health Division executive Andrew Edelsberg put things in perspective: "Only 1 in 500 firms rated A or A- can be expected to go out of business. Among those rated A+ or better, only 1 in 1,667 is likely to go bust." Busy indeed is the reader who will represent 500 carriers in his lifetime—in 2012 he would be fortunate to represent 20 LTCi carriers.

But what happens when rating agencies get it wrong? If AM Best rates a carrier too highly, and it goes into Rehabilitation, or S&P punishes a carrier with a low rating, and the company performs quite beautifully? Do consumers, journalists, or agents hold them accountable? Of course not. They may keep a rivalrous scorecard among themselves, but on Main Street there are no repercussions. Meanwhile, in an attempt to re-hydrate the letter grades into something meaningful by the use of descriptors, consider the quality of information we and our clients have been given to rely upon. AM Best, 6 gradations of "SECURE" ranging from:

- "a superior ability to meet their ongoing obligations to policholders"

- "an excellent ability to meet their ongoing obligations to policyholders"

- "a good ability to meet their ongoing obligations to policyholders"

Do the adjectives "superior", "excellent" and "good" give your prospects the information they need prior to making a 30-year commitment to a company? Knowing they do not, the agencies have offered additional qualifiers over time, including Outlook (which way the rating is trending over the next 6 months to 3 years), and Financial Size Category (based on policyholder surplus, this puts companies of similar financial capacity in the same band). Outlook is a curious thing—it’s the closest we have to a crystal ball. As a consumer, it would be best to know what the “claims-paying ability” of our carrier would be 30-years from now (when we are most likely to claim), but failing that, we’ll accept as far a look into the future as possible. But here’s the thing about the future: whether physicist or fortune-teller, no one can see into it. After studying 5-years of the publicly-available press statements of the leading rating agencies in relation to one of our leading LTCi carriers, this author made a bombshell discovery:

- In hindsight, a “negative” outlook will lead to either a “downgrade”, or a return to a “stable” outlook. In the present, we cannot determine which.

- In hindsight, a “stable” outlook can turn either “positive” or “negative”, or remain “stable” indefinitely. In the present, we cannot determine which.

- In hindsight, a “positive” outlook will lead to either an “upgrade”, or a return to a “stable” outlook. In the present, we cannot determine which.

- The different agencies do not agree with one another over the number or timing of changes. (For example, over the course of this 5-yr period one agency moved its rating of the carrier just once, even as the Comdex Score fluctuated wildly 9 times.)

WHAT A RATING DOESN'T MEAN

The concerns below are more important than "claims-paying ability" and are not denoted by the hyper-abbreviated letter grade.

- EXPERIENCE: How long has the carrier served this market? In LTCi, you can purchase limited actuarial data, but there’s no substitute for accumulating volumes of your own exclusive experiential morbidity and mortality claims data. How do you compare the B rated carrier celebrating its 25th anniversary dedicated exclusively to LTCi versus the A++ insurer whose LTCi division is younger than Pets.com?

- EXISTING CLAIMS: Who's been there? Who has the infrastructure, the staff, the processes, the case managers? Who turns their claims around in 48-hrs, who takes 7-days, and who takes 30-45 days? Ratings tell you nothing about who pays $2,300,000 each and every day like clockwork with high satisfaction ratings vs. who has yet to pay their very first claim.

- SERVICE: As an agent, you know first-hand what it’s like to work behind the scenes with each insurance company. Some are a breeze, and some make you want to pull your hair out—it will be the same for your policyholders. An A+ doesn’t tell us this.

- COMMITMENT: As you'll see below, simply having money in the bank doesn't forecast who is committed to the market, and who might exit when the seas get rough. This is a crucial but oft-overlooked point, since the carrier your client purchases from today—that A+ rated superstar—may not even be the one she files a claim with in 30-yrs. One possible lens by which to view this is to ask of the carrier, “Is LTCi a core product, a complement to their other senior portfolio, or a convenience for their career sales force?”

- AGENCY: There is no rating system for choosing insurance agencies (yet!) but consumers should invest at least as much effort into choosing their agency as their carrier. Does your agency sell 5 LTCi policies a year, 50 or 500? How strong are their testimonials and endorsements? How many claims have they assisted? How long have they been in business, and what assurance do you have that they will remain in business when you need them?

- TIMING:Hinted at earlier, let's dub this the "snapshot fallacy". It's the impression in a consumer's mind that the rating upon which she forms her opinion is "fixed" at the moment she looks. It is not. Instead, out of sight, the rating fluctuates up & down like a sine wave, while she (blithely unaware) renews her policy year after year. What would happen were she to look again in the future? If the rating she once knew as an A+ were now a B++, isn't she already locked-in? The changes serve only to cause consternation and anxiety. . . until they move back upwards, sound and fury signifying nothing.

BREAKING THE CYCLE

I acknowledge that credit ratings have their place: they affect the interest rates carriers borrow and earn on Wall Street. But I take issue with the utility of financial strength ratings as a product for Main Street. At the same time, agents are under intense pressure to reproduce ratings at the request of their prospects, who themselves were compelled to ask after having read articles by personal finance columnists, who themselves rely upon so-called "experts" and do nothing more than faithfully give space to their dogma. The cycle repeats itself like the ancient serpent eating its own tail. No one knows how to break the cycle. I get it.

When your client asks you for the AM Best rating of a carrier, how can you respectfully decline? You don't have to. I've prepared your answer:Hand your client this article to read. I've written this for all of you. After all, when analysts base their upgrades on the pre-condition that carriers successfully implement rate increases, it is consumers caught on a rope bridge burning from both ends.And what of the stellar ratings your prospects insist upon?

The following A rated carriers all voluntarily exited long-term care insurance within the past 10-years (CNA, A; Lincoln Benefit, A+; Great American, A; Allianz, A; MetLife, A+; Prudential, A+; Unum, A-; American General, A). There was no question of their financial security or stability. The rating agencies didn’t “get it wrong”. They were just irrelevant. From a claims-paying ability perspective, if we were to ask, "All things being equal, upon what else would you judge a carrier?" We have suggested experience, claims practices, administrative competence, commitment to the market, and agency support as our guides. Since the vast majority of the carriers we are all likely to represent—and our clients to choose from—are indiscernbile from a claims-paying standpoint, these should be the criteria we use today.